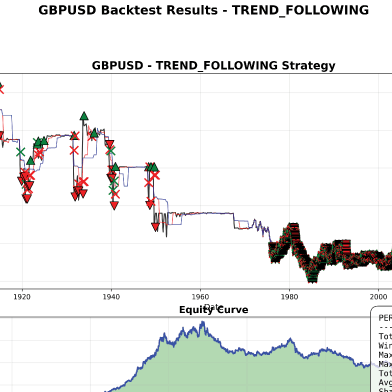

ML-Based Backtest Engine

Building a Python-based backtesting engine that automates pattern detection and validates strategies using historical statistical data instead of subjective observation.

(In development)

Manual pattern recognition in trading is often biased and lacks statistical validation. Decisions based on subjective observation limit long-term consistency.

I built a Python-based backtesting engine that automates pattern detection and evaluates strategies using historical data and machine learning models.

The result is a measurable, data-driven framework where strategies are validated statistically — not emotionally.

In development.

Drag and Drop Website Builder